PART TWO

- Feb 19

- 7 min read

Agents, disruption and the question of readiness

In December 2024, we published 'Cheaper than a Peanut' - tracking the cost of compute from $20 trillion per GFLOP in 1945 to roughly a penny. Fourteen months later, that same penny can buy you far more. The peanut was a metaphor. But that metaphor is now too expensive.

And as a result there are no longer waves of progress. They have united as converging exponentials: cost collapse, efficiency breakthroughs, benchmark annihilation, coding automation. There is only a single wall of water is now to be seen.

This essay is a continuation of Part 1, which we recommend you read first. Enjoy!

THE AGENT ERA ARRIVED

If cost collapse was the energy building beneath the waves uniting into a single surface of water, the rise of autonomous agents is the leading edge of the single wave as it now presents - the first visible sign of what is starting to make landfall across every industry.

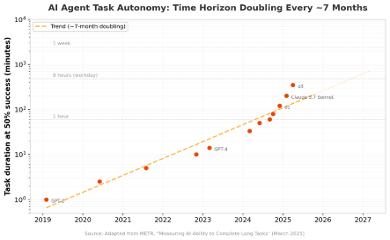

METR published the defining quantitative chart of 2025 in March: the time horizon of tasks AI agents can autonomously complete has been doubling every seven months over the past six years, with evidence suggesting acceleration to roughly every four months in 2024–2025. On a log scale, the line is nearly vertical.

Figure 6: METR’s task autonomy time horizon - the “most misunderstood graph in AI” (source: METR, March 2025; adapted)

As of early 2025, frontier agents could autonomously complete coding tasks that take humans over six hours, at 50% reliability. If the trend holds, agents capable of week-long autonomous projects could arrive within two to three years. The agent market, estimated at $5.4 billion in 2024, is projected to reach $47–53 billion by 2030. PwC’s May 2025 survey found 79% of organisations have adopted AI agents to some extent.

Two complementary protocols now form the plumbing of a multi-agent world. Anthropic’s Model Context Protocol (MCP), launched in November 2024, standardises how agents connect to tools - the “USB-C port for AI.” Google’s Agent-to-Agent Protocol (A2A), announced in April 2025 with 50+ launch partners, enables agents from different vendors to discover and coordinate with each other. Together, they make agent-to-agent collaboration a near-term reality rather than a theoretical possibility.

KNOWLEDGE WORK FACES ITS MOST DISRUPTIVE MOMENT

McKinsey’s November 2025 report Agents, Robots, and Us delivered the most striking revision in recent consulting history: 57% of U.S. work hours could now be automated with currently demonstrated technologies - nearly double the 30% they had estimated for 2030 just two years earlier. AI agents alone could handle tasks occupying 44% of work hours. The economic value potential: approximately $2.9 trillion in the U.S. alone.

Figure 7: McKinsey doubled its automation estimate in just two years (source: McKinsey, November 2025)

Enterprise adoption has moved rapidly. 88% of companies now use AI in at least one business function, up from 55% in 2023. 72% of workers use AI regularly. AI fluency demand grew 7× in two years, from roughly one million workers needing the skill in 2023 to seven million in 2025. In legal, 85% of lawyers now use generative AI daily or weekly. In finance, 98% of North American banks use AI in at least one process. In customer service, AI resolves 65% of queries without human intervention, with first-response times plunging from six hours to under four minutes.

But the gap between potential and realisation remains wide. Only 5–6% of companies generate meaningful value from AI at scale. 84% have not redesigned roles. 42% of companies abandoned most AI initiatives in 2025. The technology has arrived; the organisational transformation has barely begun. This gap represents both the risk and the opportunity for firms prepared to act.

THE LEADERS CONVERGE ON AN EXTRAORDINARY TIMELINE

“AI is now writing much of the code at Anthropic, it is already substantially accelerating the rate of our progress in building the next generation of AI systems. This feedback loop is gathering steam month by month, and may be only 1–2 years away from a point where the current generation of AI autonomously builds the next.”

- Dario Amodei, “The Adolescence of Technology,” January 2026 (5.7 million views)

The statements from AI leaders since December 2024 form a remarkable convergence. Amodei predicted in March 2025 that “powerful AI systems will emerge in late 2026 or early 2027” - systems with intellectual capabilities matching or exceeding Nobel Prize winners across most disciplines.

Sam Altman wrote in January 2025: “We are now confident we know how to build AGI as we have traditionally understood it.” Jensen Huang declared at GTC 2025 that the industry has reached a “$1 trillion computing inflection point.”

The International AI Safety Report, led by Yoshua Bengio with backing from 30 countries, found in February 2026 that AI capabilities are “improving faster than many experts anticipated” and current risk management is “insufficient.” The United States declined to back the 2026 edition - a departure from its support for the 2025 report.

THE WORLD IS NOT READY

In the original Cheaper than a Peanut, we argued that organisations needed to grasp the trajectory or risk being overtaken. Fourteen months on, the concern has shifted from organisational readiness to societal readiness. The people who build AI are increasingly alarmed by how few of the people who will be affected by it are engaged in preparing for its arrival.

“I think there needs to be more time spent by economists, probably, and philosophers and social scientists on what do we want the world to be like, even if we get everything right, post AGI. I’m surprised there’s not very much discussion about that, given the relatively short timelines.”

- Demis Hassabis, Axios interview, February 2025

Hassabis, a Nobel laureate who arguably has as clear a view of the trajectory as anyone alive, has returned to this theme repeatedly. At the Paris AI Action Summit, he warned that international cooperation on AI governance is becoming harder, not easier: “It seems to be very difficult for the world to do. Just look at climate. There seems to be less cooperation. That doesn’t bode well.” In a TIME interview, he was blunter still: “We need some great new philosophers” to grapple with what happens when labour automation removes the economic leverage that underpins democratic societies. “I think the top economists should be thinking a lot about this.”

He is not alone. The International AI Safety Report, backed by 30 countries and led by Yoshua Bengio, concluded in February 2026 that AI capabilities are “improving faster than many experts anticipated” and current risk management remains “insufficient.” The United States declined to back the 2026 edition - a departure from its support just twelve months earlier. At Davos in January 2026, Hassabis noted that even with the best technical safety, the societal challenge remains enormous: “We don’t have a lot of time to sort out before we get to AGI.”

This is not a call for pessimism. It is a call for engagement. The data in this paper shows that AI is transforming knowledge work faster than any prior technology. McKinsey doubled its automation estimate in two years. AI coding agents went from prototype to $1 billion in revenue in six months. Benchmarks designed to last years fell in months. The wave is not on the horizon any more. It is overhead. And the institutions responsible for education, regulation, workforce transition, and social safety are, for the most part, still standing on the beach.

THE MONEY FOLLOWED THE EXPONENTIAL

Total AI venture capital roughly doubled from $100–114 billion in 2024 to $202–270 billion in 2025, with AI capturing over 50% of all global VC for the first time. Foundation model companies raised $80 billion, more than doubling from $31 billion the year before. The mega-rounds were staggering: OpenAI ($40B from SoftBank), Anthropic ($13B at $183B valuation), xAI ($10B equity plus $3.5B debt at $200B). These are not speculative bets on a distant future. They are infrastructure investments in a transformation that is already underway.

Figure 8: AI venture capital and hyperscaler CapEx, 2020–2025 (sources: Crunchbase, Goldman Sachs, company earnings)

Revenue growth has been hyperbolic. OpenAI scaled from roughly $200 million ARR in early 2023 to $13 billion by August 2025 - a 65× increase in 29 months. Anthropic went from $87 million to $7–9 billion in under two years. NVIDIA posted $130.5 billion in FY2025 revenue, became the first company to reach $5 trillion market capitalisation, and controls 86% of the AI chip market.

Combined hyperscaler CapEx from Amazon, Microsoft, Google, and Meta surged to roughly $405–443 billion in 2025 - a 62–73% year-over-year increase. Goldman Sachs projects $1.15 trillion over 2025–2027. The Stargate Project committed $500 billion to AI infrastructure. But a concerning 10:1 spend-to-revenue ratio persists: AI cloud services generated roughly $25 billion in revenue against $240 billion in CapEx. J.P. Morgan estimates $650 billion in annual AI revenue is needed to deliver a 10% return on the cumulative buildout.

WHAT WE NOW KNOW

First, the pace is compounding. Epoch AI found that post-January 2024 inference prices dropped at 200× per year, versus 50× for the broader period. The METR doubling time may have compressed from seven months to four. Benchmark improvements in the November–December 2025 explosion exceeded full-year gains from prior years. This is not a steady exponential - it is a steepening one.

Second, efficiency is the new frontier. DeepSeek demonstrated that algorithmic innovation can substitute for brute-force compute at a 10–20× ratio. A 3.8-billion-parameter model now matches what required 540 billion parameters in 2022 - a 142-fold efficiency gain. Karpathy can reproduce GPT-2 for the price of a pub lunch. The open-source performance gap narrowed from 8% to under 2% in a single year. The cost to match yesterday’s frontier falls faster than the cost to push tomorrow’s rises.

Third, the transformation is real but unevenly distributed. McKinsey’s upward revision from 30% to 57% of work hours automatable is seismic. AI coding agents hit billion-dollar revenue milestones. But only 5–6% of companies generate meaningful value from AI, 84% haven’t redesigned roles, and 42% abandoned most initiatives in 2025. The technology is here. The organisational and human adaptation is not.

Sources and methodology: This paper draws on Stanford HAI AI Index 2025, Epoch AI inference pricing analysis (March 2025), METR “Measuring AI Ability to Complete Long Tasks” (March 2025), Andreessen Horowitz “LLMflation” (November 2024), McKinsey “Agents, Robots, and Us” (November 2025), BCG “AI at Work 2025,” SemiAnalysis “Claude Code Is the Inflection Point” (February 2026), Andrej Karpathy’s nanochat/llm.c GPT-2 reproduction series (2024–2026), GitHub Octoverse 2025, the International AI Safety Report (February 2026), Crunchbase annual data, company earnings reports and investor presentations, and public statements from the leaders of Anthropic, OpenAI, Google DeepMind, xAI, Meta, Microsoft, and NVIDIA. Chart data has been reconstructed from published figures and may contain minor approximations. All charts are original recreations by Brightbeam for this publication.